Uncertain Times? Consider Investing in Real Estate Debt

March 2, 2020

With low interest rates and the recent volatility in the stock market and economy at large, many investors are increasingly focused on more defensive investment opportunities which can potentially hedge against uncertainty. As a result, institutional and individual investors alike are looking beyond equity and investing in commercial real estate debt.

Within the U.S., this sentiment has fueled an increase in demand for debt financing, through which investors participate in the financing of loans to property owners or sponsors. Such commercial real estate loans have typically been funded by traditional lenders such as banks and life insurance companies, increased regulation over the past decade has curtailed the scope and amount of lending these institutions can deploy. As a result, a FDIC report released late last year shows non-bank mortgage servicing quadrupling between 2008-2018, as evinced in the graph below.

Source: FDIC Quarterly, November 2019

With investors increasingly financing commercial real estate loans, debt funds have continued to gain share across all real estate project types. According to a recent study by firm Real Capital Analytics, debt funds now account for 22% of U.S. construction lending and 21% of value-add project lending, as illustrated below.

Source: RCA Insights, October 2019

As a result, mortgage brokers and borrowers underserved by the traditional funding sources are increasingly being funded by alternative lenders who have stepped in over the past few years to fill the funding gap.

Below, we discuss the primary advantages commercial real estate debt financing can confer to investors and give an overview on iintoo’s newest offering in this space.

The Benefits of Commercial Real Estate Debt Financing

With real estate debt investments, investors act as lenders to property owners, developers or real estate companies sponsoring deals. The loan is secured by the property, and investors earn a fixed return based on the loan’s interest rate and the amount they’ve invested. Real estate debt can be an attractive investment for several reasons:

- Risk mitigation: In a debt deal, investors typically have priority over other investors when it comes to interest or principal payments. As a result, investors take on less risk with debt investments relative to making a full equity play, and under a debt deal structure the loan is typically secured by the property, which acts as collateral against repayment of the principal.

- Income stream: Real estate loans pay a either fixed or variable rate depending on the deal terms, which enables investors to expect a steady stream of income.

Not All Debt is Created Equal

When choosing between allocating capital towards debt or equity investments, real estate investors must be clear about what they want to prioritize in terms of potential for higher returns versus relative security and predictability. For investors who are keen on diversifying their portfolio or taking up a more defensive approach to real estate investing, it’s also crucial to understand the differences between the two most common forms of debt in this space.

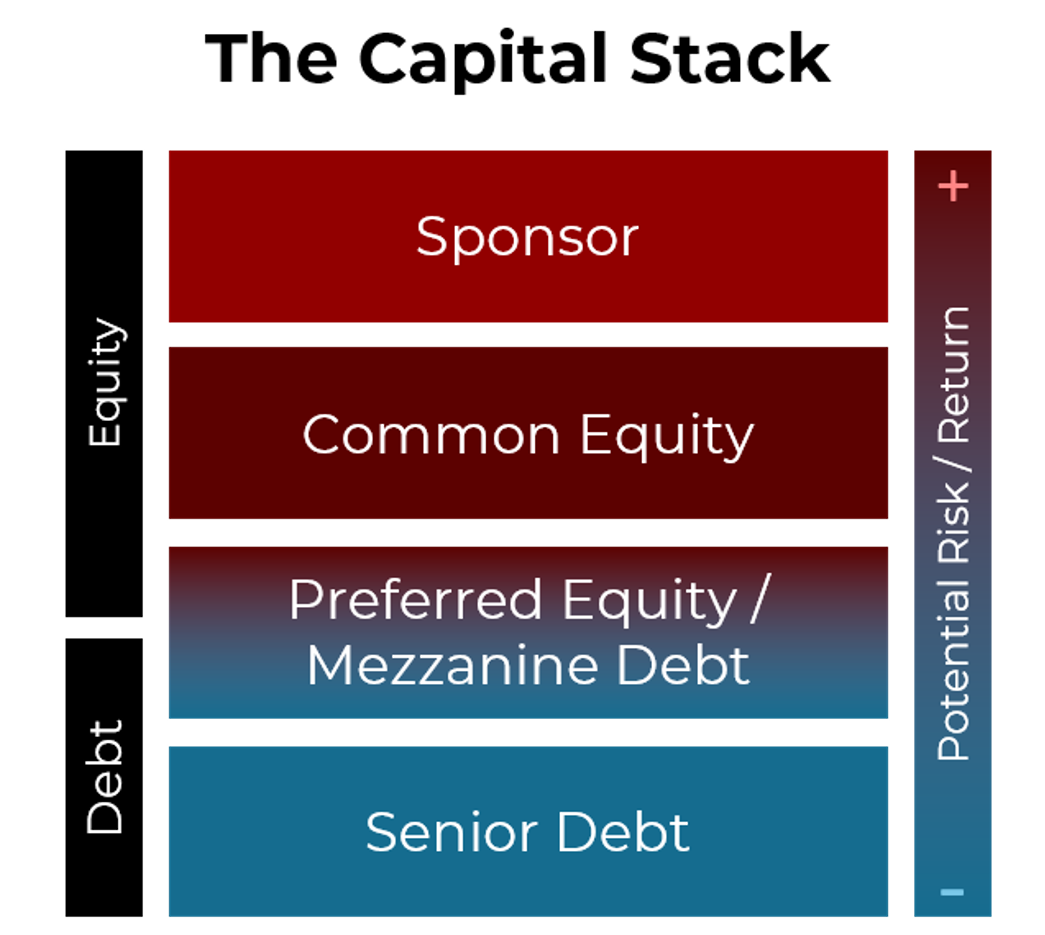

Senior secured debt: Senior, or unsubordinated, debt sits at the foundation of the capital stack and typically constitutes the largest part of the stack. This debt is usually a mortgage secured by the property and is also called a senior secured loan or a first lien loan, since lenders who own the first mortgage on a property own the first lien.

In the event of nonpayment, lenders typically have the right to force the sale of the property to cover the outstanding obligation, making this the most secure type of debt. This requires an understanding of a deal’s loan-to-value ratio (LTV).

The LTV ratio measures the loan amount as a percentage of the collateral property’s value. For example, if a lender’s maximum LTV ratio is 60%, that means they are willing to give a loan up to 60% of a property’s value. Therefore, the maximum loan the lender will make on a $3M property would be $1.8M. As a result, if adverse market conditions result in a depreciation of the $3M value of the underlying asset, the lender has a $70,000 cushion to cover market fluctuations. Therefore, the smaller the LTV, the larger the cushion to protect investors in the event of a loan default.

Mezzanine debt: Also known as subordinated debt, mezzanine debt is typically used to bridge the gap between institutional loans and shareholder equity. This type of debt sits a level above senior debt on the capital stack, which means they are paid out only after the borrower services its senior debt and pays all operating expenses involved in the project.

Introducing iintoo’s Senior Debt Financing

Investors who want to increase their exposure to real estate while diversifying their portfolios can now invest in senior secure debt.

Our recently launched Alternative Investment Fund (AIF) is currently invested in ~300 non-bank senior debt loans across a diverse set of real estate projects across the U.S, and iintoo investors benefit from the AIF’s proprietary risk measurement model, which offers both geographic diversification and a mix of asset types. These short-term loans are secured by first lien on the underlying asset, which gives our lenders first position seniority. And since the average LTV of the loans in the Fund is currently below 60%, iintoo investors’ capital will take priority even if the average sale price of properties within the Fund is up to 40% below projection.

From a long-term perspective, diversification is a sound approach to balancing risk and reward in a real estate portfolio. To this end, commercial real estate debt investing can be a good fit for certain investors.

And as a senior-positioned, fixed-income vehicle that produces cash income from the inception of the investment, iintoo’s AIF provides a compelling value proposition to investors and is a strong addition to our diverse selection of investment opportunities.

To learn more, feel free to take a closer look at our current offerings.